The last date to file your income tax returns is July 31 each assessment year. However, if you missed the deadline, don’t worry! There’s always hope. The Income Tax Act offers a couple of solutions: belated returns for those who missed the original deadline and revised returns for those who want to update their existing returns. Have a quick read as we outline each detail, including the filing process, penalties, and interest implications down below.

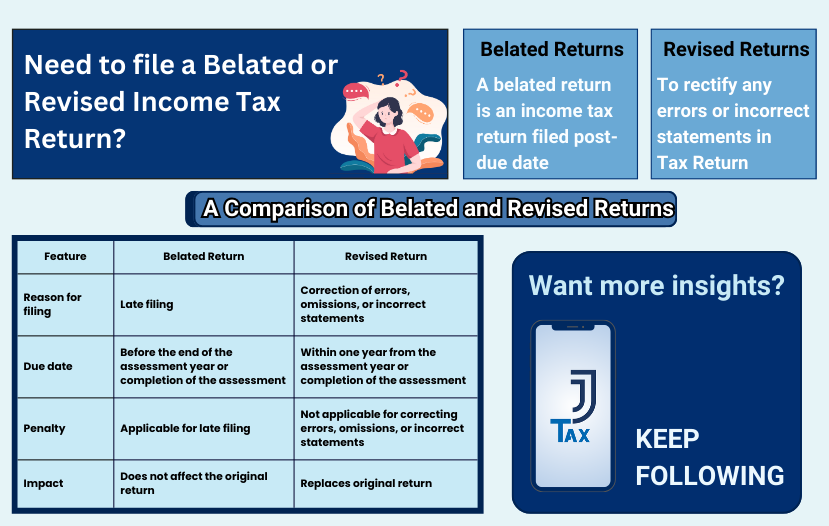

In simple terms, a belated return is an income tax return filed post-due date but before the end of the relevant assessment year or the completion of the assessment, whichever is earlier. The due date for filing income tax returns is dependent on the taxpayer's status and the nature of their income. The 31st of July is the D-day for salaried individuals and self-employed professionals. But for companies and individuals requiring tax audits, the deadline is extended to September 30th.

However, it is prudent to know that filing a belated return can result in financial penalties. In the current income tax regime, individuals who file their returns after the due date but before December 31st are liable to pay a penalty of ₹ 5,000. Thereafter, the penalty rises to ₹ 10,000. These penalties apply only to those individuals with a total income of over ₹ 5,00,000. If you fall below this slab, the penalty is reduced to ₹ 1,000.

It is only human to make mistakes while filing your ITRs, no matter how carefully you do it. Further to rectify any errors, omissions, or incorrect statements in an original or belated income tax return, you can always file a revised return. Be aware that this provision is applicable only for unintentional mistakes and does not allow for concealment or false statements. The revised return must be filed before the expiry of one year from the relevant assessment year or before the completion of the assessment, whichever is earlier.

A taxpayer may file a revised return multiple times as there are no limits for revision. However, the revised return will supersede the original return, and any carry-forward losses or income calculated in the revised return will be applicable going forward. It should be noted that a revised return cannot be used to change the status or accounting year of the taxpayer or to alter the method of accounting.

Apart from the procedures or circumstances highlighted above, there are a few more scenarios where filing a belated or revised return might be necessary.

Job loss or reduction in income: If you experience a significant decrease in income or face unemployment, you need to file a revised return to reflect your accurate income for the year.

Sale of assets: The sale of assets such as property or investments during the year requires the profits or losses to be reported on your income tax return. If you omitted or misreported these transactions in your original return, you may need to file a revised return.

Changes in tax laws: Modifications in the tax laws may have an effect on your tax liabilities. File a revised return to reflect the impact of these changes.

A belated or revised return is a viable provision for those who have missed the deadline or need to correct errors in their income tax returns. Timely and accurate tax filings can help avoid any unnecessary penalties and future hassle. We hope this blogpost highlighted the specifics related to both which might help you whenever you are in a related situation. And just in case you need any more guidance, feel free to download the JJ Tax app which offers expert solutions to all your taxation and compliance requirements you may have.

.jpg)