Understanding the Ins and Outs of Taxation on Retirement Income 👴🏻👵🏻

Peek into the profound principles of pension taxation, where precision and prudence play a pivotal role.

Unravel the mysterious world of income tax on pensions with us - it's like solving a puzzle that leads to more cash in your stash!

We want to make this topic easy to grasp and empower you with valuable insights. Whether you're approaching retirement, already enjoying its benefits, or planning for the future, understanding pension taxation is vital.

Are Pensions Taxable?

The amount received by an employee on retirement is called Pension.

In the realm of taxes, pensions are akin to a salary when you file your Income Tax Return (ITR). There are two types of pensions; commuted and uncommuted pensions.

According to the rules set forth in the Income Tax Act of 1961, an uncommuted pension, that is, a pension plan not yet converted into a lump sum, falls under the category of salary. As a diligent pension earner, you'll need to file your ITR accordingly.

Now, let's decode the terms. An uncommuted pension grants you the flexibility to receive periodic payments, usually on a monthly or a quarterly basis. However, do keep in mind that such periodical pension payments are fully taxable as salary.

On the other hand, if you opt for taking a lump sum amount as pension, it is known as commuted pension.. The commuted pension enables you to receive a portion of your pension in advance.

Let’s understand this through an example:

For instance, your pension amount is INR 20,000 per month. Now, you choose to receive 20% of your pension for the next 10 years in advance as lumpsum pension.

So, 20% of (INR 2,40,000*10) = Rs 4,80,000 is your commuted pension which will be paid to you in advance.

For the same 10 years, you will receive Rs 16,000 (80% of INR 20,000) as uncommuted monthly pension and from 11th year, you will be paid full pension of Rs 20,000 on a monthly basis .

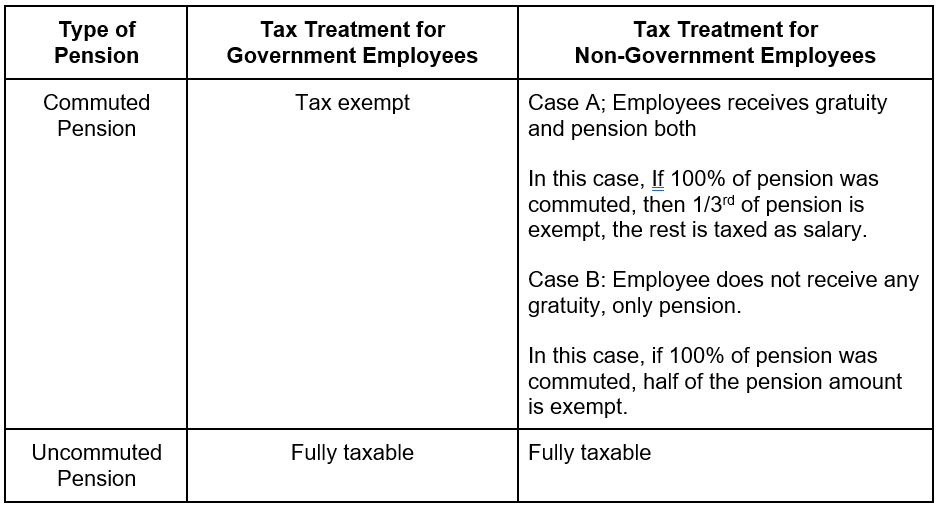

Tax treatment of different types of pensions

When it comes to pensions, understanding the tax treatment can be like deciphering a complex code. Let's unlock the secrets of taxation for different types of pensions:

● Government Pension: Pensions received from the central or state government fall under the "Salary" category in your Income Tax Return (ITR). Uncommuted pension is fully taxable. However, commuted pension received by employees of State Government, Central government or defense forces is fully exempt. Make sure to account for this income while filing your ITR..

● Private Sector Pension: Pensions received from private companies are also taxable and should be included under the "Income from salary" section in your ITR. Since pensions received from private players is taxable.

The employer will deduct Tax Deducted at Source (TDS) on your pension income, and it's essential to reconcile the TDS amount while filing your ITR to ensure proper compliance.

● Family Pension: Family pension is granted to the legal heirs of a deceased person who was receiving a pension. It is considered as "Income from other sources" in your ITR. The tax liability on family pension is determined by the applicable income tax slab rate for the recipient. Take note of this while preparing your ITR to ensure accurate tax calculations.

The taxability of commuted and uncommuted pensions varies for government and non-government employees.

Taxes on pension received by a family member

When a family member receives a pension, it is considered as "income from other sources" in their income tax return. The tax treatment depends on whether the pension is commuted (turned into a lump sum) or uncommuted (received as regular payments).

● Commuted Pension: If the pension is converted into a lump sum payment (commuted), it is not taxable in the hands of family member. They get to keep the entire amount without any tax implications.

● Uncommuted Pension: If the pension remains as regular payments, it is partially exempt. This pension is taxable after allowing a deduction of INR 15,000 or 33.33% of the uncommuted pension amount, whichever is less. This deduction is also available to the pensioners who opt for New Tax regime.

For example, if a family member receives a pension of INR 1,20,000, they will get a deduction of least of the two: INR 15,000 or INR 40,000 (33.33% of INR 1,20,000). Thus, the taxable family pension will be Rs. 1,05,000 (INR 1,20,000 - INR 15,000).

Bottom line

To make the most of your pension and avoid any surprises at tax time, keep these points in mind. Being informed and careful with your pension can help you secure a better financial future.

Rest assured, at JJ Tax, we've got your back every step of the way! Our team of experts is dedicated to making pension taxation a breeze for you, ensuring you sail smoothly through the process.

May your retirement be taxing in all the right ways, with a pension that's filled with joy and financial ease!