Learn the role of GST in buying and selling of properties.

For crores of aspiring homeowners in India, the dream of owning a piece of real estate has got a layer of complexity. The Goods and Services Tax (GST), implemented in 2017, has significantly revamped the financial landscape, and the real estate sector is no exception. While the pre-GST regime saw a plethora of taxes levied at various stages, GST promises a more streamlined system. But did it translate into lower costs for homebuyers?

This newsletter delves into the intricacies of GST in real estate transactions, dissecting the implications for different property types, potential cost changes, and other considerations for navigating this new landscape. Whether you're eyeing a swanky apartment in Mumbai or a cosy villa in Goa, understanding GST's impact is paramount to making informed decisions and potentially securing savings on your dream home.

For Indian homebuyers, the Goods and Services Tax (GST) has emerged as a key factor influencing property transactions.

Pre-GST Maze: Before GST, homebuyers faced a mix of taxes levied at various stages of a property purchase. These included excise duty on building materials, value-added tax (VAT) on construction services, and service tax on developer margins. The effective tax burden could vary significantly depending on the location and type of property.

GST Reshapes the Landscape: GST ushered in a more transparent system with distinct tax brackets for different property categories. However, navigating these brackets requires a keen eye:

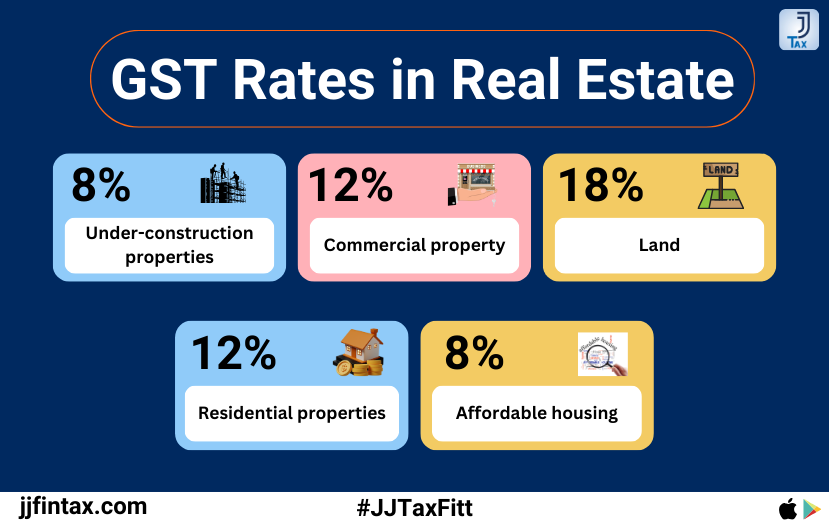

Under-construction Properties, particularly those catering to the affordable housing segment through credit-linked subsidy schemes, have emerged as the clear winners. The pre-GST regime levied a cascading effect of taxes, with excise duty on building materials, VAT on construction services, and service tax on developer margins pushing the effective tax burden upwards of 8%.

GST on an Under-Construction commercial property is 12%. However, under GST, a single rate of 12% applies on under-construction properties, whereas no GST applies on completed or ready-to-sale properties, only if the Completion Certificate (CC) has been issued.

In March 2019, the GST Council cut the tax rates to 5% from 12% on residential properties and 1% from 8% for the affordable housing segment. However, ITC benefits will not be available under the new tax rate policy.

Ready-to-Move-In Properties: Unlike their under-construction counterparts, ready-to-move-in properties (both residential and commercial) are generally exempt from GST. However, state-levied stamp duty remains a cost factor to consider. While this might appear advantageous on the surface, don’t forget that stamp duty, a state-level tax, still applies. Depending on the location and property value, stamp duty can range from 2% to 8%, potentially negating any perceived benefit from the absence of GST.

Resale Properties: For resale properties, the tax implications become more intricate. Here, the focus shifts to the nature of the transaction:

Land Purchase and Sale: This falls under the purview of works contract, attracting a GST rate of 18%.

Composite Supply: This umbrella term encompasses various scenarios. Resale properties can be part of a composite supply, with a GST rate of 18% for regular transactions, 12% for sales to government authorities, and again 12% for supplies meant for the general public. Notably, affordable housing resale under the composite supply framework also attracts a concessional rate of 12%.

The Goods and Services Tax (GST) has cast a long shadow on India's real estate sector, presenting a mixed bag of implications. While streamlining the previous tax structure was a welcome change, the impact on affordability and developer margins remains a subject of debate.

For homebuyers, the potential for cost savings is a glimmer of hope. Under-construction properties, particularly those falling under the credit-linked subsidy scheme for affordable housing, now benefit from a concessionary GST rate. This translates to a potential reduction in the overall tax burden compared to the pre-GST era. However, for developers, the story is more complex. The pre-GST regime allowed them to claim Input Tax Credit (ITC) on various inputs used in construction. Under the current system, while ITC remains available, the inverted duty structure in certain segments, where the tax rate on raw materials is higher than the final sale price, can lead to accumulated credit that cannot be readily utilized. This can strain developer cash flow and potentially impact project timelines.

Despite these initial challenges, the long-term outlook for GST in real estate appears promising. Increased transparency in the sector, a hallmark of GST, can foster greater trust between buyers and developers. Additionally, the streamlining of tax processes can potentially reduce administrative hassles for developers, leading to improved efficiency. Ultimately, the success of GST in the real estate sector hinges on a multi-pronged approach. Addressing the concerns of developers regarding ITC accumulation, while ensuring the benefits of the streamlined system reach homebuyers, will be crucial in unlocking the full potential of GST for a more vibrant and transparent Indian real estate market.

For businesses navigating the complexities of India's Goods and Services Tax (GST), having a thorough understanding of Input Tax Credits (ITCs) is important. This mechanism serves as a cornerstone of the GST framework, enabling businesses to claim tax refunds on purchases used for making taxable outputs. In essence, it prevents the cascading effect of taxes, where a tax is levied on top of another previously paid tax.

Say a manufacturer producing goods with a final selling price of Rs. 500. Under GST, the manufacturer is liable to pay a tax, say, Rs. 500, on the final sale. However, during the production process, the manufacturer incurs various expenses like raw materials and machinery, each subject to GST. Let's assume the total tax paid on these inputs amounts to Rs. 300. Here's where the ITC comes into play. The manufacturer can claim an ITC of Rs. 300, effectively reducing the final tax liability to the government. In this scenario, the manufacturer would only need to pay Rs. 200 (Rs. 500 output tax - Rs. 300 ITC). This ensures that the tax burden falls solely on the value added at each stage of production, fostering a more efficient tax system.

The eligibility to claim ITCs extends beyond manufacturers. Businesses registered under the GST Act, including suppliers, agents, aggregators, and e-commerce operators, can all leverage this mechanism. By claiming credit for taxes paid on qualified purchases, businesses can significantly reduce their overall tax outgo, enhancing cash flow and potentially influencing pricing strategies. However, it's crucial to note that specific rules and regulations govern the eligibility of ITC claims, and adhering to them is essential for businesses to optimize their tax benefits under the GST regime.

India's Goods and Services Tax (GST) has introduced a potential cost advantage for buyers of luxury apartments. The current regime imposes a 5% GST rate on luxury housing, which might seem like a welcome reduction compared to pre-GST tax structures. However, it's important to note that this benefit comes with a caveat – unlike some other purchases under GST, the tax paid on luxury apartments cannot be offset by claiming Input Tax Credit (ITC). This means the overall tax saving might be less significant than initially perceived.

While the 5% GST rate on non-affordable housing offers some relief, the true focus of the GST regime in the housing sector lies in its support for government-led affordable housing initiatives. Recognizing the need for wider access to homeownership, the government has implemented a significantly lower 1% GST rate for these projects. This translates to substantial cost savings for eligible beneficiaries, making their dream of owning a home more attainable.

The real winners under GST seem to be those seeking affordable housing. The government's commitment to this segment is evident in the significantly lower 1% GST rate for these projects, translating to substantial cost benefits for eligible homebuyers.

As the GST regime continues to evolve, policymakers face a delicate balancing act: ensuring affordability for aspiring homeowners while fostering a sustainable tax environment for developers catering to this vital social need. Here's where a trusted tax advisor like Uniqey by JJ Tax can be invaluable.

Uniqey by JJ Tax, with its team of experienced professionals, possesses a deep understanding of the intricacies of GST as it applies to the housing sector. We can help both buyers and developers navigate the system, maximizing potential tax benefits and ensuring compliance. We believe informed decision-making is key to success in this dynamic market.

While the market may fluctuate, Uniqey by JJ Tax helps you build a solid foundation of knowledge with clear and concise communication. Let's craft your tax strategy together.

Looking ahead, the housing sector's response to the differential GST structure will offer valuable insights into the effectiveness of the tax reform in achieving broader economic goals in India.

.jpg)